B. Com. - Bachelor of Commerce 6th Semester

Direct Tax Law

Paper-BCM-601

Time Allowed: Three Hours] [Maximum Marks: 80

Note:-Unit-I: Attempt four questions out of six questions, each carries 5 marks.

Unit-II: Attempt two questions out of four questions, each carries 15 marks.

Unit-III: Attempt two questions out of four questions, each carries 15 marks.

UNIT-I

1. Write a note on Deemed Income with example.

2. The particulars of Assessment Years 2020-21 and 2021-22 are as under:

Compute the total income for each Assessment Year.

3. Briefly explain the procedure for claim of rebate u/S 86.

4. The following particulars have been submitted by Mr. Y in the capacity of Karta of a Hindu Undivided Family for assessment purpose:

(a) Profit from family's business Rs. 2,50,000, after charging an amount of Rs. 60,000 given as salary of Karta's brother who has been actively participating in it.

(b) Salary income of Karta's another brother who is a Manager in a Co-operative Bank Rs. 11,000 p.m.

(c) Director's Fee received by Karta Rs. 5,000 (HUF holds 20% shares in this company).

(d) Bank interest on fixed deposits Rs. 24,000.

(e) Long-Term Capital Gain from transfer of building Rs. 28,000.

(f) Long-Term Capital Gain from the transfer of investment Rs. 40,000.

(g) Donation to a College which is an approved institutio Rs. 40,000.

(h) Rental Value of the property let Rs. 36,000, Municipal

Tax paid in respect of the house Rs. 4,500. Interest on loan taken for repair of house is Rs. 12,000.

You are required to calculate total income and tax liability of the family for the Assessment Year 2021-22.

5. Define an AOP. Also explain with help of a numerical rates prescribed for assessment of AOP.

6. Profit and Loss Account of ABC and Co. (Chartered Accountant firm) for the year ending 31-3-2021 is as follows:

Other Information:

(1) Out of expenses of Rs. 10,000, Rs. 6,400 is not deductible by virtue of Section 36 and 37.

(2) Depreciation as per Section 32 is Rs. 27,500.

Find out the amount of total income of the firm for the Assessment Year 2021-22. The remuneration and interest on Capital to Partners have been paid according to Partnership Deed, which was submitted along with return.

UNIT-II

7. What are the provisions of law regarding the clubbing of income of spouse and other family members in the income of individuals?

8. Mr. B furnishes following information regarding his profit or loss from various business activities and other incomes and losses for the year ending on 31st March, 2021:

(1) The Net Profit as shown in the P & L A/c of textile business Rs. 4,15,600. Following additional information available from P & L A/c are:

(i) Depreciation debited Rs. 1,02,000 whereas depreciation calculated as per Income Tax rules comes to Rs. 81,000.

(ii) Interest from Bank deposits credited in P & L A/c Rs. 28,000.

(iii) Income from sale of scrap credited Rs. 37,600. (iv) Rent received from workers who were given some part of business premises on rent Rs. 12,000.

(v) A gift of Rs. 10,000 was given to Mr. A's wife on Diwali and is debited to P & L A/c.

(vi) Income Tax paid debited to P & L A/c is Rs. 14,800.

(2) Profit from Cycle business Rs. 2,24,000.

(3) Profit from speculation business Rs. 1,60,000.

(4) Loss from gambling Rs. 42,000.

(5) Speculation business loss b/f from Assessment Year 2015-16 Rs. 2,10,000.

(6) He retired from Central Govt. job in 2012 and he received pension of Rs. 4,80,000 during the previous year.

(7) During the year, he spent Rs. 80,000 on the medical treatment of his dependent ailing mother suffering from a specified disease. She is 75 years old.

(8) He is paying Rs. 60,000 per annum on the medical insurance of himself, spouse and dependent father.

(9) His savings during the year are as under:

(i) Deposits in PPF Rs.1,20,000.

(ii) Life Insurance premium paid on the life of his dependent son, spouse and himself Rs. 48,000.

(10) During the year he spent Rs. 72,000 on travelling sightseeing places in India.

Calculate his total income.

9. What are those circumstances in which Assessing Officer can take the action to determine income from transaction with non-residential to avoid tax?

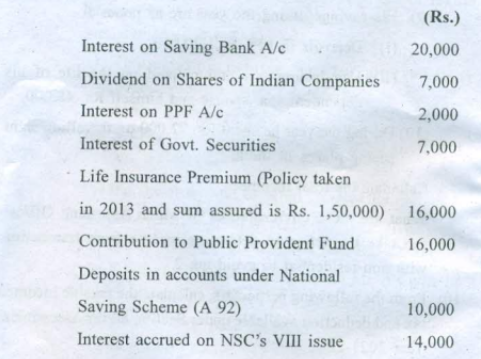

10. From the following particulars, calculate the taxable income, tax and deduction available under Section 80 for Assessment

Year 2021-22: (Rs.)

Salary per month 15,000

Dearness Allowance per month 10,000

House Rent Allowance per month 3,000

(Rent paid Rs. 4,000 pm)

House property is let out on a monthly rent of Rs. 2,000. The annual value of the house property is Rs. 30,000. Municipal Tax paid is Rs. 1,800 for whole year. Interest Payable on Capital borrowed for the construction of the house is Rs. 6,000. Repayment of house buildings loan taken from friends is Rs. 5,000 and from Life Insurance Corporation is Rs. 3,000.

UNIT-III

11. What do you understand by Best Judgement Assessment? Under what conditions is it made by the Assessing Officer? On what grounds can a Best Judgement Assessment be cancelled?

12. Rakesh and Ram are members of an AOP sharing profits and losses in the ratio of 2:1. AOP has income of Rs. 2,63,000 under the head profits and gains. It also has agricultural income of Rs. 90,000. The individual income of its members are as follows:

During the year Rakesh paid ULIP of Rs. 7,500 and Ram paid Rs. 3,600 by cheque under Mediclaim and deposited Rs. 7,500 in PPF. Calculate the tax liability of AOP and its members for the Assessment Year 2021-22.

13. What are the different penalties which can be imposed under the provision of Income Tax Act, 1961?

14. Anita, Beena, and Chitra are Partners in a firm assessed u/S 185 sharing profits and losses equally.

Their capitals were: Rs.

Anita 20,000

Beena 30,000

Chitra 10,000

The Profit and Loss Account of the firm for the previous year ended 31st March, 2021 showed a net profit of Rs. 10,000 after charging the following items:

(1) Salary to Anita Rs. 300 per month and to Chitra Rs. 500 per month.

(2) Interest on Capital at 6% per annum.

(3) Rent to Anita Rs. 150 per month in whole building business was carried on.

(4) Interest on loan taken from Beena Rs. 500.

Compute the total income of the firm.

0 comments:

Post a Comment

North India Campus